If you are a current bank employee, a new entrant to the workforce or simply curious about digital transformation, this blog series is perfect for you. In this blog series, we will explore the digital banking landscape, types of skills needed and where to obtain these skills. In the first article of the series, we will go through the latest FinTech trends and how it impacts your career. This series will be released weekly, so be sure to check them out. Let us jump right into it!

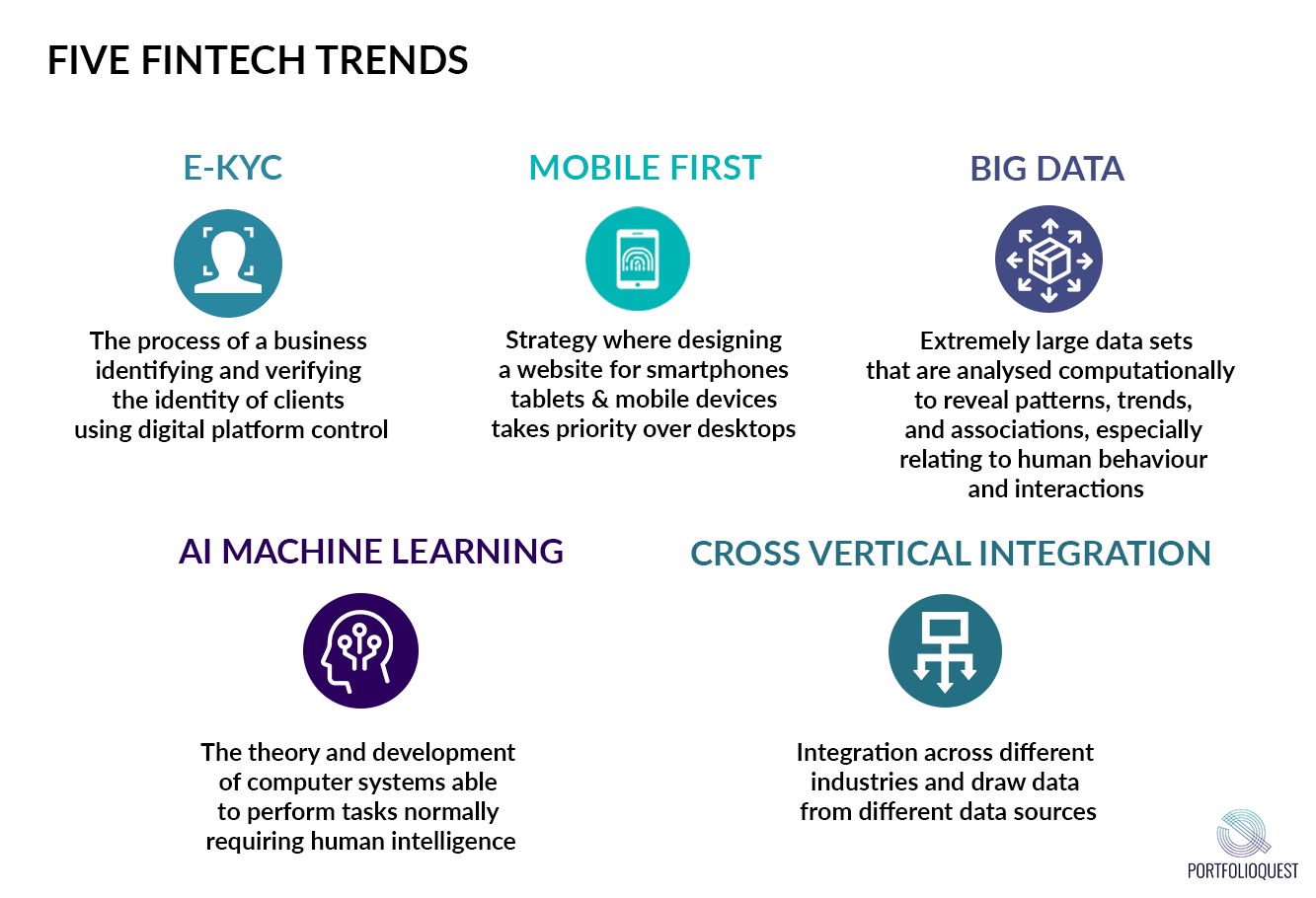

- E-KYC

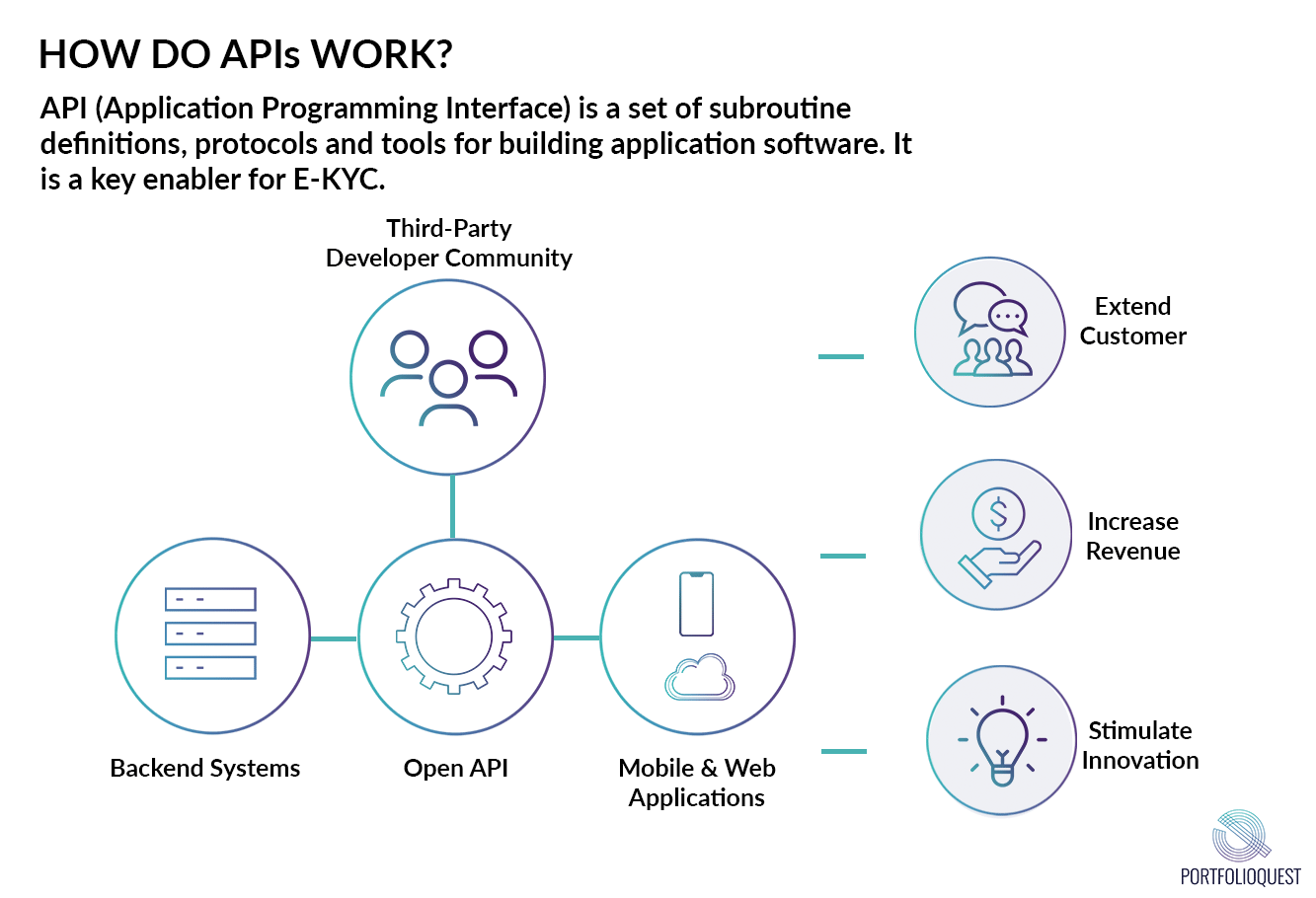

A key enabler of E-KYC is the Application Programming Interface (API), which is a set of subroutine definitions, protocols, and tools for building application software. Some common examples of E-KYC currently used are biometrics (facial recognition), voice control (Siri) and fingerprint.

Due to its increasing adoption in different industries, it is important to understand how APIs fundamentally work. Many would be familiar with Apple Pay, which uses your fingerprint to log in. Capital One, a bank in the US uses open APIs to authenticate credit cards through Alexa. An active bounty program to make sure that businesses are able to use APIs to streamline authentication will be necessary.

If you are not familiar with APIs, a good place to start is to try every possible API and biometric option for yourself as a customer. This will give you a broad understanding of how APIs work and keep you updated on the latest API trends.

- Mobile First

It is not about the device, it is about the data! Simply digitizing the old process is not going to help you win but rather starting the whole approach from the phone is key.

DBS launched its first digital-only bank in India that is branchless and paperless by leveraging on biometrics and artificial intelligence. N26 and Monzo are truly disruptive, fully digital banks that fundamentally do things differently from a bank. With the phone becoming the device of choice for the majority of the people, mobile payments are making fast inroads due to such an availability. Smartwatch payments are the next big thing where you can simply wave your NFC powered smartwatch over a POS machine at the shop to make a payment. On a side note, understanding data privacy laws and playing by the rules becomes especially important with this new development.

The increasing adoption of mobile payments would make keeping up with government and industry initiatives for UPI, NFC, and other mobile payments systems especially important.

A key differentiating factor that characterizes big data is that the data sets are so voluminous and complex that traditional data processing application software is inadequate to deal with them. According to IBM, the large amount of unstructured data can be leveraged to better meet customer needs, optimize operations and infrastructures as well as find new sources of revenue.

For example, Starbucks rewards its 13 million customers when they download the app and use it to make purchases. This allows them to generate huge amounts of data through linking customers with the products and traffic data. As such, the marketing function at Starbucks could utilize such data accumulated to better understand the purchasing behaviour of their customers and roll out targeted advertising and discounts. Big data could provide useful information to convert customers from disloyal to loyal.

Although there are packages with machine learning type capabilities to handle unstructured data, they are still largely limited. Data visualization will be an important skill as large amounts of big data will need to be distilled and analyzed. You will also need to stop yourself from over-using the excel graph buttons but instead “up your game” with a data visualization approach.

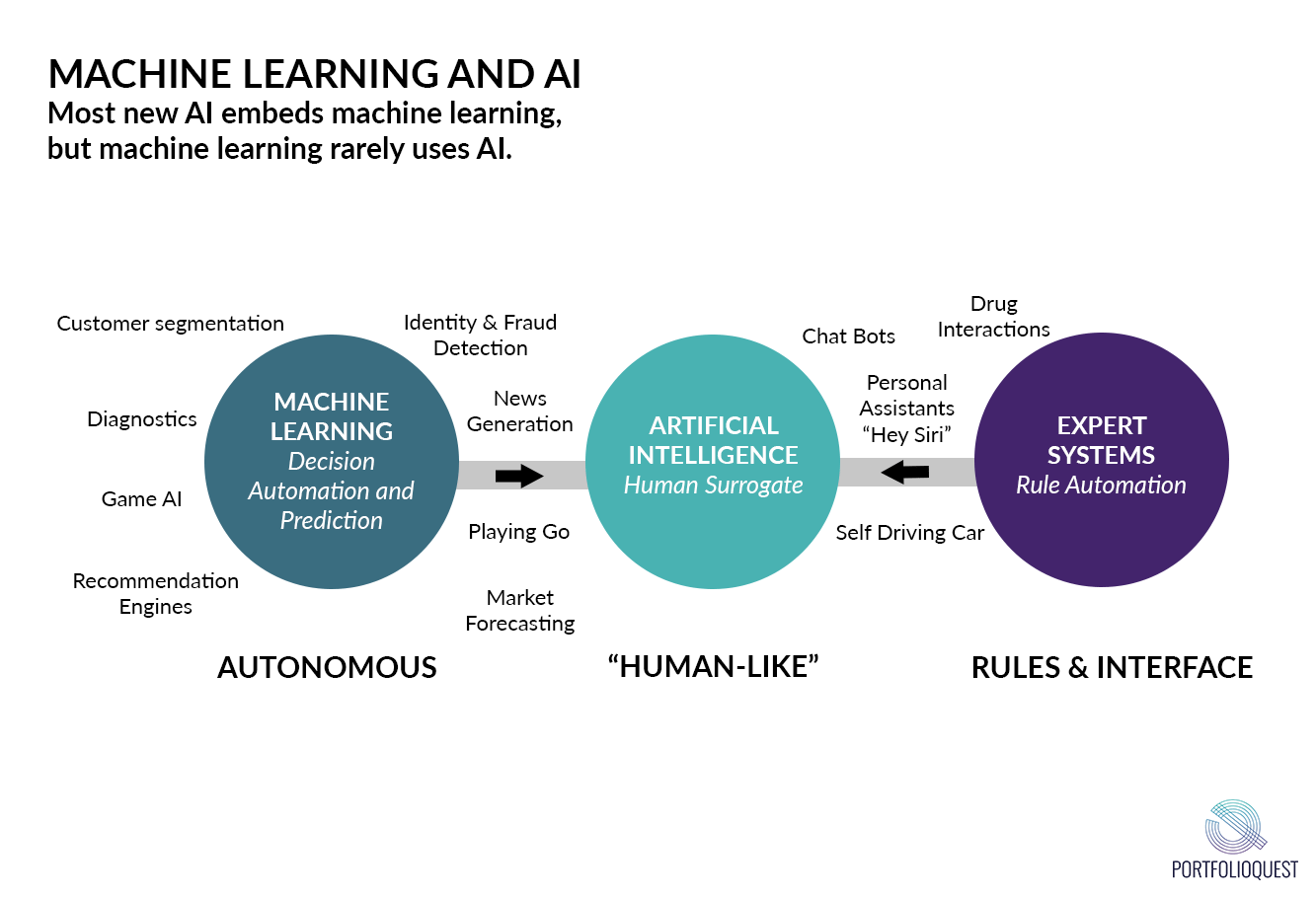

They are perhaps the most used buzzwords in recent times but there are some distinctions between the two. Expert systems are rule-based automation that is heavily used in the financial sector. Machine learning consists of supervised and unsupervised learning, in which cluster analysis is used. AI is the next step after this, where anticipation is involved, which makes it more “human-like”.

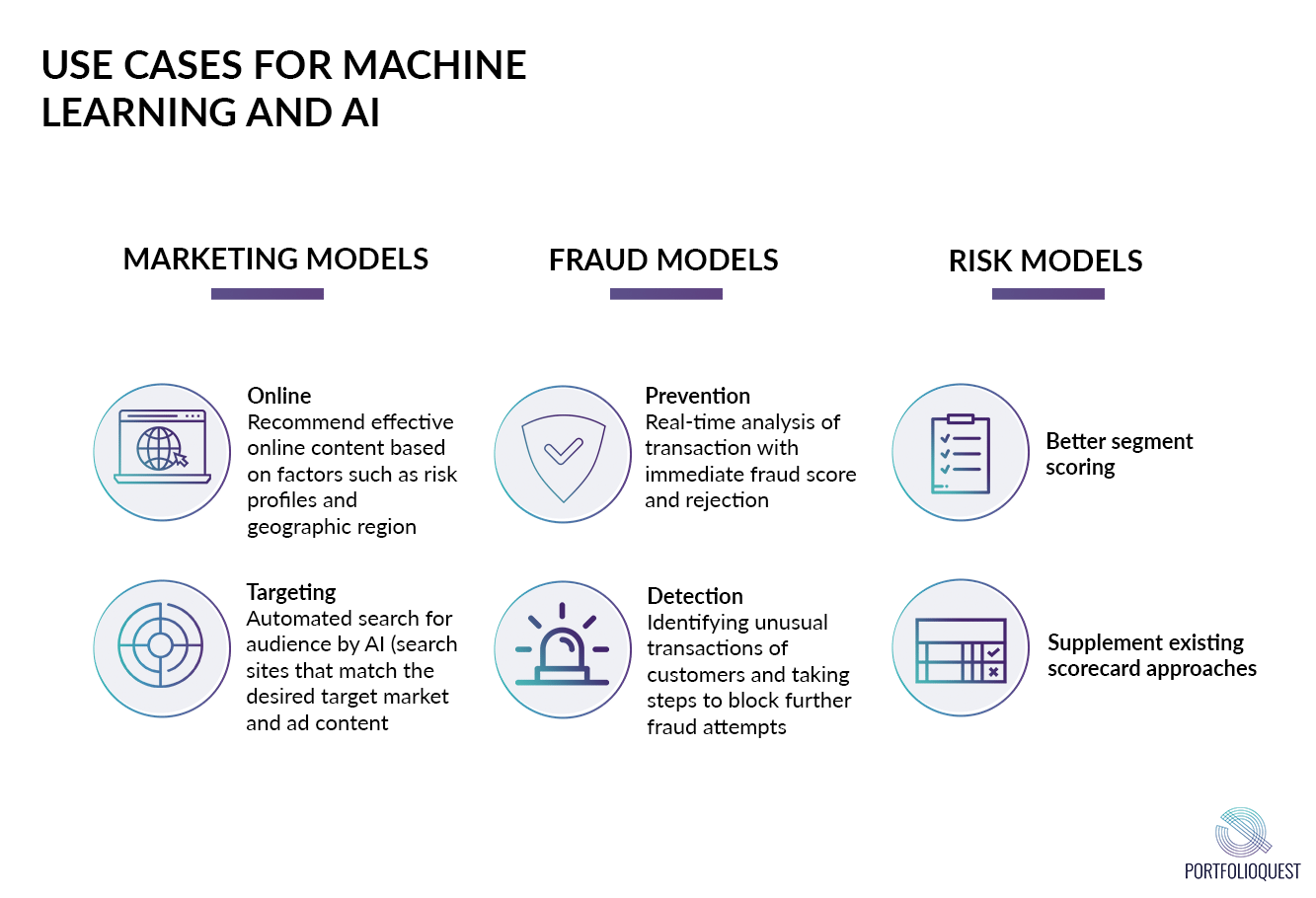

For example, an internet credit service company in China pulls in different data sources and offer easy money installment payments with their point of sale lending. The biggest ROI comes from the marketing and risk models. For marketing, at any given moment, 1200 active machine learning models are in production to identify customers, make offers, and communicate with them. Machine learning will enable richer classification with the multiple data sources.

AI is a cool buzzword, but “stay in your lane” with machine learning most of the time. Starting with descriptive statistics and graphics will help you really understand what you have at hand. Being able to bring together the different data sources and get a good result will make you a valuable entity in any business.

- Cross Vertical Integration

Integration across different industries will provide many data sources to draw from. For example, GrabPay is a payment function that uses the ride-hailing application as a wallet, with various promotions to encourage people to put money in the wallet. This allows Grab to watch spending patterns of users. Amazon bought a physical store because this allows them to acquire customer behaviour data.

Given the trends, building corporate partnerships that are data gold mines, monetizing and utilizing the data in an important way will be crucial to a business’ success. Apart from forming strategic partnerships, consumer, e-commerce and marketing trends are slowly being integrated into retail banking and wealth management. For instance, how quickly people are moving to wearables will inform how quickly banks need to move to a wearable application.

Think outside the box; a FinTech career step might be in e-commerce or in marketing due to the rich exposure to data. You can test out every shopping or travel application to find out what kinds of data they are getting from you.

At the end of the day, the person who can integrate the data is going to win. These are huge trends but in isolation, they are not going to get you there. Being able to combine the pieces and have a use case is key. Data skill sets become critical.

The blog post is inspired by the “Five FinTech Trends in Retail Banking and Wealth Management” webinar by Michelle Katics. You can download the slides here.

In the next article, we will explore the differences between working in a traditional bank and a digital bank. Stay tuned for that!

Pingback: Future-Enabled Digital Banking Skill Sets You Need to Have

Pingback: Life Hacks for Ongoing FinTech Education and News